Estrategia de inversión

7 ago. 2026

Eye on the Market

PERSPECTIVAS 2022

La reactivación económica: Endgame

Haga clic en cada superhéroe de la reactivación para leer más

Michael Cembalest

Chairman of Market and Investment Strategy for J.P. Morgan Asset & Wealth Management

INTRODUCCIÓN

Estos superhéroes contribuirán cada uno a su manera a la subida de los precios y de los salarios, del crecimiento económico y de los precios de los activos. En el artículo de Perspectivas de este año analizamos las consecuencias de la reactivación económica para los mercados de renta variable, que ya han descontado gran parte de las buenas noticias. Los temas especiales incluyen China y su purga regulatoria, la inversión orientada a los dividendos, los activos reales (inmobiliario comercial, madera e infraestructuras), inversiones en fintech y en empresas de ciberseguridad, el impacto de las consideraciones ESG en las carteras y el alto coste del Brexit.

-

Renta variable cotizada: Dividendos, ciberseguridad y fintech

-

1Dividendos de la renta variable: Nos guste o no, los dividendos son un elemento esencial de la inversión orientada a las rentabilidades

-

2Inversión en ciberseguridad: cuando se juntan la innovación y la maldad, surgen oportunidades para los inversores

-

3Fintech también puede ser sinónimo de miedo, fraude y ejecuciones hipotecarias

-

4Los elementos fundamentales del mercado de oficinas en Estados Unidos ya están mejorando, a pesar del COVID

-

5Inversión en infraestructuras: El diablo está en los detalles (distribución eléctrica, energía solar y almacenamiento al por mayor)

-

6Madera: Rentabilidades estables con un posible recorrido alcista en un mundo que busca la captación efectiva de carbono

-

7Continúan las inversiones en China, a pesar de la purga regulatoria y la ralentización del crecimiento en 2021

-

8Brexit y el alto precio de la soberanía nacional

-

9Los beneficios de los factores ESG para las carteras parecen más claros, pero son anteriores a la recuperación en 2021 de los sectores de energía tradicionales

Leer o escuchar las Perspectivas de 2025

ETIQUETAS

Compartir

ESCUCHAR PODCAST

[START RECORDING]

FEMALE VOICE: This podcast has been prepared exclusively for institutional, wholesale, professional clients and qualified investors only, as defined by local laws and regulations. Please read other important information which can be found on the link at the end of the podcast episode.

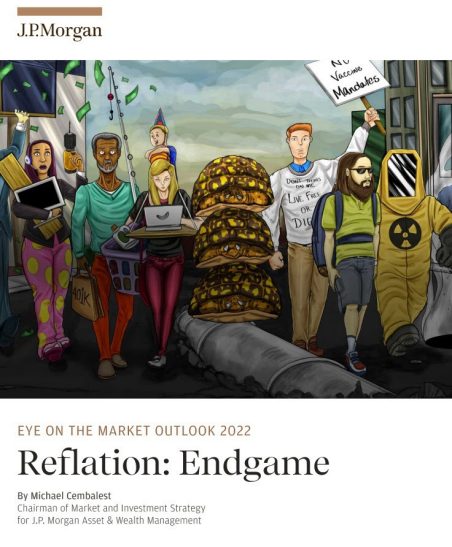

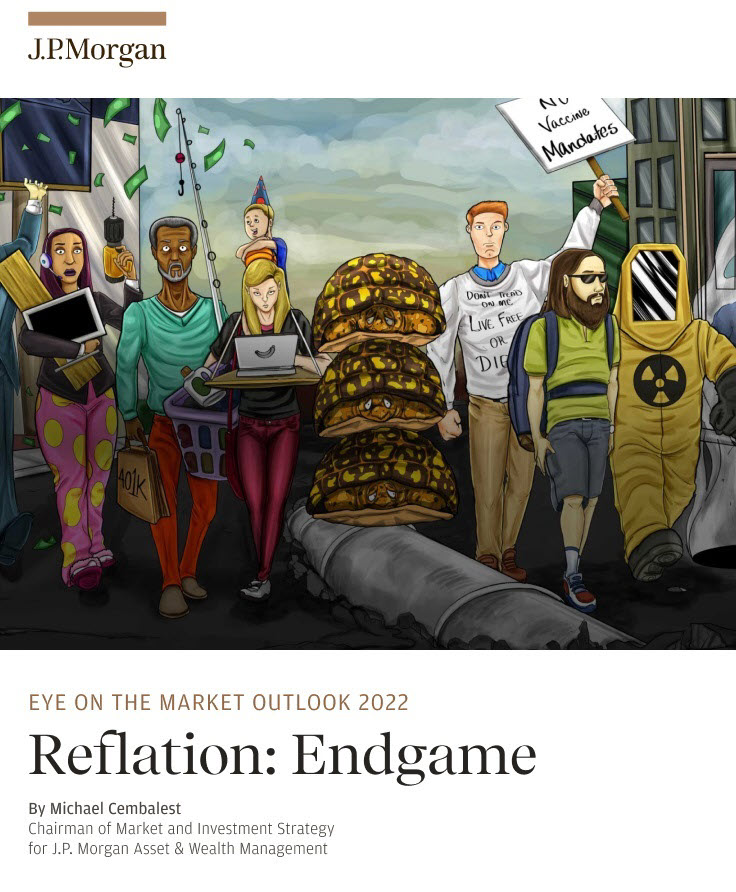

MR. MICHAEL CEMBALEST: Happy New Year, everybody, and welcome to the 2022 Eye on the Market Outlook, which is entitled Reflation Endgame. I’ve never actually seen a superhero movie, but I can imagine what they look like, and I’ve seen the posters for them. So the poster for this year, the cover art for this year’s Eye on the Market, is a group of superheroes, all of whom are contributing in one way or another to rising prices, wages, nominal growth, and asset prices.

And you take a look at the cover art, you’ll see politicians who are creating the largest monetary and fiscal stimulus on record, the impact from all the work-from-home employees that are driving up demand for import and semiconductor-intensive goods, which are worsening supply chain bottlenecks, the big jump in retirees taking advantage of rising home prices and rising 401(k) account values, working mothers, millions of whom are still having trouble finding childcare and the impact that has on the labor markets, the oil and gas and coal producers who have reverted into their shells, they’re depicted as turtles.

Capital spending in new projects for thermal power have fallen by 75%, even though the demand for thermal energy hasn’t really moved much at all. We’ve got a vaccine resistor on the cover and the obvious impacts that has on the labor force, other labor force dropouts and switchers, healthcare regulators passing vaccine mandates, and then one of the other last but important impact on the labor market is about a million in the US missing immigrant workers in the US labor supply. And that follows on the Trump era when immigration fell to its lowest level since the 1980s.

So all of these factors are part of the reflation endgame that’s the theme of this year’s Executive Summary, and we walk through the consequences for equity markets that are already pricing in plenty of good news. The structure of the outlook is always an Executive Summary, and it gets followed by some specific investment topic discussions. This year we review China and the regulatory purge and the prospect for investing there in 2022, what the landscape looks like for dividend investors, and then we take a look, a deep dive into some real asset topics, commercial real estate, office specifically, and the trends taking place there, infrastructure and timber. We also look at investments in Fintech and cybersecurity. And lastly, from a policy perspective, we look at ESG impacts on portfolios and what is now emerging is the pretty high cost of Brexit.

In the Executive Summary, we review the story that you’re all familiar with, with the COVID recession having recovered so quickly to eliminate spare capacity now at a faster pace than prior recessions. We have global inflation close to the highest level in 20 years, which is driven by a number of things, surging goods prices, changing consumption patterns, the inability of adjusted time corporate sector to respond to that, soaring government debt and monetary policy that dwarfs anything we’ve ever seen. And then energy policies which reduce the supply of thermal energy faster than they reduced demand.

And so as the year came to an end, we saw some weakening manufacturing indicators. Normally that’s a negative sign for investors, but this time around, the supply chain shocks, I think, were more responsible for these weakening manufacturing indicators. And that’s why we’re optimistic that with gradual resolution over some period of months of some of the supply chain delays, global growth is going to rebound. And we’re already starting to see, in both the US and Europe, a shift back towards services from goods spending, which was one of the main catalysts for some of these supply chain problems. We’ll see what happens as Omicron rolls through and it may be a temporary reversal. But the bottom line is that the pig through the snake in terms of this surge in goods spending relative to services appears to be abating in the developed world.

Now, I won’t go into the details here, but we do have a page on some of the supply chain issues. This is not just the byproduct of COVID and the shift in spending. There’s a lot of structural issues in the US that are that are negatively affecting the supply chains in terms of local regulations. I won’t go through them all here, but you’ve got to look at this page. No port in the US ranks in the top 50 globally in terms of cost or more important, efficiency and speed. These Los Angeles ports that you read about all the time rank 328 in the world, and Long Beach comes into 333. There are contracts that prevent port automation. There’s limits on operating hours; there’s weekend closures. And the semi-automated Port of Virginia doesn’t have any backlogs and ranks, comes in at about 85. But there’s a lot of issues here in the US that this supply chain stuff has surfaced, which are structural and not just cyclical.

Anyway, we walk through a lot of the usual suspects that we’re tracking regarding some of these supply chain issues, which are still obviously on the high side as we enter the year. The question is how do they get resolved. And if you look historically, there have been some pretty severe supply chain issues that have taken place in the past. And normally what happens is they get resolved within a few months as capital spending catches up to demand. And COVID is a complicating factor, but we expect that to happen this time as well.

A pretty good example of that is the, what now looks like a very large increase in automobile-related semiconductor capital spending, which is expected to double next year versus prior trends, and this is pretty critical for supply chain given the rising number of semiconductors per car. We have a chart in here that looks at semiconductor values per car and the overall automotive electronics cost per car. So with a lot of the goods supply chain issues, eventually we expect capital spending to help resolve some of those shortages in addition to increased vaccination rates in Asia and a gradual reduction in some of the shipping costs.

The challenge here is that while we think that the goods supply chains are going to get better, there are still two problems that we think are going to get solved much more slowly, and the first one of those is obviously labor. US labor shortages appear to be a real chronic issue, driving up wage inflation, very tight labor markets. Last October, we walked through the seven to eight million people that are missing from the labor force for different reasons, whether it’s accelerated retirement, changes in immigration rules, increased self-employment out of large cities, vaccinated people afraid to return to work, working parents can’t find childcare, unvaccinated people that are fired or furloughed from their jobs. The bottom line is the latest data from the BLS shows low-skill wages rising at almost 7% a year. And what we end up with is the tightest labor markets in well over 30 to 40 years.

Now we still don’t know what’s going to happen to the reconciliation bill, given the objections from Manchin, but we could have as much as $2 trillion deployed as direct government purchases and other indirect government purchases. At a time of very tight labor markets, I’m not sure exactly where all the workers are going to come from and what impact that will have on wages at a time of very tight labor markets. So while the goods supply chain issues should resolve themselves over the next two months, the labor ones I don’t think will.

And then again, as I mentioned earlier, energy-related inflation may be pretty sticky. And there has been a massive collapse in oil and gas production investment at a time that global demand for fossil fuels has barely declined. And for everybody that would like to see more rapid de-carbonization, you have to match the decline in the supply and demand of something, or else the price is simply going to go up and you’re going to end up with more imports.

An extreme version of this is found in Europe. Electricity prices are soaring to kind of preposterous levels because their renewable energy policy changed faster than underlying fossil fuel demand and given its reliance on Russia for half of all of its thermal energy needs. If you think US electricity prices are high, just look at the chart here on page ten, which looks at the day-ahead electricity prices in France, Spain, and Germany. They’re somewhere between six to eight times higher than what they are in the United States per kilowatt hour.

So I’ve summarized a lot of the Executive Summary here, and there’s a lot of other topics we discussed. But the bottom line is that the Fed is now facing the largest challenge yet to its description of inflation dynamics being transitory. We agree with the Fed that goods price inflation should roll over in the next few months, but I think, we think that wages and commodity prices are going to remain high because those supply/demand curves have shifted.

So what does all of that mean? The important question we think you have to ask is what’s the Fed’s end game? In prior cycles, the end game was a policy rate above the rate of inflation and meaningfully above the rate of inflation. We think the Fed’s end game in this cycle is going to be a policy rate which more or less reaches inflation. In other words, in real terms, rates would still be zero. And part of that has to do with a new approach the Fed has been using to think about what’s the right level of equilibrium policy rates.

So for investors, that means that 2022 might not be as disruptive as you might think in a year of Fed tightening, because the end game here is still very, very favorable for risk-taking because you’re talking about real rates of around zero rather than a real rate of something between 1 and 1.5, or maybe even 2%. And while the Fed is expected to scale back its asset purchases, the J.P. Morgan economists think there’s going to be another $1 trillion in developed markets central bank balance sheet expansion in 2022, so you’re still going to have support from other central banks.

Boiling it all down, we expect 2022 to be a miniature version in the equity markets of 2021, meaning last year we had massive earnings growth of 33%, a fairly large PE multiple decline of 8 to 10%, and then that offset to deliver a pretty nice return. We expect something like 10 to 12% or maybe 13% earnings growth this year. We expect PE multiples to contract again, as they did last year, the net result being something like a 7 to 10% return on the S&P, including dividends.

And part of the headwind there is that in 2021, profit margins were extremely high, mostly because companies passed along cost increases to consumers. We think we’re getting close to the limits of that, and we may actually see margins fall by 1% or so back to where they were in 2017 to 2019.

So it looks to us like a year of, let’s say, 7 to 10% returns. But it’s important to recognize that some of the market internals are a lot less favorable than they were last spring, and we expect there to be some fairly big bumps in the road during the year, and that you should retain some liquidity in anticipation of those. So let me just tick through some of them. There’s a lot of young unprofitable companies out there. They make up the largest share of market caps since 1999. There’s a lot of supply coming from these young unprofitable companies, whether it’s through primary or secondary issuance or insider lockups expiring, that can weigh on the market.

There’s a lot of companies that are now more sensitive to changes in liquidity conditions than economic conditions. That can weigh on the market. There’s a lot of concentration of S&P market cap in total return that’s very reliant to a handful of stocks. And the last point I’d make here is that there are some obvious signs that the momentum plays and the crowded trades are beginning to weaken. Just look here on page 13 at the chart on Fintech, renewable energy, IPOs in general, SPACs in particular. You’re starting to see a lot of those momentum liquidity-crowded trades perform very weakly. So this is a sign to us, all of these things I’ve just mentioned, that we’re going to have a lot more volatility in 2022 than we did in 2021, and people need to be prepared for that.

One last comment on equities. A lot of our clients are always looking for deep value. Now you should all be aware looking for deep value ten years into a monetary policy regime of zero interest rates is not likely to deliver very much to you, right? In other words, everything has been picked over like a Thanksgiving carcass at 1:00 in the morning. But if you are looking for deep value, there’s not very much the. The three places you’ll find it, and we talk about this in more detail on the page 14, is large cap pharma, biotech, and airlines. Each one of those three has their own very specific challenges that explain why they’re trading at deep value levels. Of the three, large cap pharma looks the most interesting to us.

In the special topic sections, there are three main categories, public equities, real assets, and policy issues. Within public equities, we talk about the landscape for dividend investors. Kind of sparse, but there are some things to take a look at. We talk about cybersecurity, where the need for additional cybersecurity investment just continues to skyrocket.

There are some interesting charts here in terms of thinking about the impact of COVID on the cybersecurity industry. When you look at the impact of COVID specifically, there has been a big jump in the share of overall customer interactions, products, and services that are now digital compared to in-person when compared to pre-COVID. And so obviously that creates even more importance for cybersecurity measures and companies and the products and services that they provide.

We have an interesting discussion here on Fintech. And look, we’re big Fintech fans. In our wealth management business, we designed investment products to focus on both public and private Fintech companies. And they’re valued higher than traditional banks despite the fact that at an industry level, the profitability is similar on it when you’re looking at return on equity.

There were three tomatoes that one can throw at the Fintech industry during COVID that we walk through here that I think are important to watch. The Fintech lenders completely disappeared during the early stages of the pandemic. They had an unbelievably high estimated incidence of fraud during all the PPP loans. And there is some evidence that Fintech lending resulted in some much more poorly underwritten loans with greater risk of default than traditional banks. And this evidence during the COVID period builds upon prior research showing greater systemic risks from Fintech lending in general. So we’re watching, we’re still enthusiastic about the sector, but we’re watching to see what impact some of these things might have on the regulatory oversight of the Fintech companies.

Within the real assets section, we take a look at commercial office. I’m surprised to see it already. There’s a huge bid offer between employees and management with respect to what the future of work looks like. But what I’m surprised to see here is that there are signs in the US that the office market fundamentals are already improving in terms of absorption of vacant and sublet space. So we kind of talk through that. I guess the good news about this whole issue is that office markets in general are much less important than they used to be for most institutional and high net worth investors as office shrinks as a component of an overall diversified commercial real estate portfolio.

We’ve got a long section here on infrastructure investing. And what I wanted to do is get into some of the details of how these projects actually work, how they generate cash flow, how they protect themselves from disruptive change and things like that. So I won’t go into the details here, but we did a deep dive on one of our electricity distribution projects, on a contracted solar power project, and another one in bulk liquid storage. And I think what you’ll see here that’s interesting as a common denominator is the degree to which these projects rely on taker pay contracts which reduce sensitivity to economic growth and other structural changes.

And then there’s a timber section in here which I spent a bit of time on. Timber investing is a fairly mature industry, and the harvesting yields themselves are fairly predictable. And we walk through the history of timber investing and how it works and things like that, and fire risks and insect risks and investing outside the US, et cetera, and potential demand from cross-laminated timber.

We conclude though with an interesting discussion on optionality from timber. There’s a lot of companies that have made commitments regarding their emissions and appear to be relying on accomplishing that through direct air capture, carbon mineralization and all sorts of other things like that, which exist primarily today on cocktail napkins. I think they’re in for a rude awakening because a lot of these things require massive amounts of energy and cost to perform, and I think a lot of them are going to end up eventually figuring out that buying trees to monetize the unharvested carbon sequestration is the better way to go.

The last section looks at some policy issues, and China needs more time than I can give on a quick 15 to 20-minute podcast. The bottom line is that we think the positives are going to outweigh the negatives as it relates to the onshore Chinese stocks next year. There are still plenty of negatives. The antitrust regulators are still on the march. There are a lot of restrictions in terms of overseas listings and higher compliance costs. China is not really providing too much help to defaulting property developers. Zero COVID policies constrain growth. The Olympics are coming up, which means you may have anti-pollution policies which still bite.

But the bottom line is we think that you’re starting to see pro-growth statements and allowances for greater credit allocation and things like that, which should make 2022 a better year. J.P. Morgan Equity Research, for example, expects around 20% earnings growth, almost 5% real GDP growth, and just 2% inflation. And if that happens, investors should benefit.

So that’s it for this podcast. Thank you for those of you that have been listeners to it. I look forward to maybe seeing you in the New Year as we maybe start moving around a little bit more. Of course, with respect to COVID and the Omicron variant and what we know about the duration of efficacy and all sorts of other things, please see our virus web portal. The Omicron section is section five and goes into details on all the trends and things that we now know. And the short answer is yes, it is much more transmissible and communicable than all the other variants, but there are early signs that the risk of hospitalization is significantly lower than other variants. Although once you are hospitalized, the risks appear to be somewhat the same as Delta. Anyway, enough for now. Thank you for listening, and let’s hope 2022 is in some ways an easier year for all of us than 2021. That’s it, bye for now.

FEMALE VOICE: Michael Cembalest’s Eye on the Market offers a unique perspective on the economy, current events, markets and investment portfolios, and is a production of J.P. Morgan Asset and Wealth Management. Michael Cembalest is the Chairman of Market and Investment Strategy for J.P. Morgan Asset Management and is one of our most renowned and provocative speakers. For more information, please subscribe to the Eye on the Market by contacting your JP Morgan representative. If you’d like to hear more, please explore episodes on iTunes or on our website.

This podcast is intended for informational purposes only and is a communication on behalf of J.P. Morgan Institutional Investments Incorporated. Views may not be suitable for all investors and are not intended as personal investment advice or a solicitation or recommendation. Outlooks and past performance are never guarantees of future results. This is not investment research.

[END RECORDING]

Acerca de Eye on the Market

Michael Cembalest es presidente de Estrategia de Mercados e Inversiones de J.P. Morgan Asset Management. Desde 2005, es el autor de Eye on the Market, que abarca una amplia variedad de temas sobre mercados, inversiones, economía, política, energía, financiación municipal y mucho más.

Archivos de Eye on the Market

Estrategia de inversión

4 ago. 2026

Rotación en el mercado: ¿qué desafíos se está encontrando la inversión en IA?

Información importante

Este artículo utiliza protocolos de seguridad rigurosos para datos seleccionados obtenidos de operaciones de tarjetas de crédito y de débito de Chase para asegurar que toda la información se mantiene de forma confidencial y segura. Todos los datos seleccionados han sido altamente agregados, y toda la información identificable, incluyendo nombres, números de cuentas, direcciones, fechas de nacimiento y números de Seguridad Social, ha sido retirada de los datos antes de que los reciba el autor del artículo. Los datos de este artículo no son representativos de la población total de titulares de tarjetas de crédito y de débito de Chase.

Las opiniones y las estimaciones que se expresan en este artículo constituyen la opinión de Michael Cembalest, basada en las condiciones actuales de los mercados, y están sujetas a cambios sin notificación previa. La información incluida en este artículo podría diferir de las opiniones expresadas por otras áreas de J.P. Morgan. Esta información no constituye de ninguna manera investigación de J.P. Morgan y no debería ser tratada como tal.

Consideramos que la información que se recoge en este documento es fiable; sin embargo, no garantizamos que sea completa o exacta. Las opiniones, las estimaciones, las estrategias y las perspectivas de inversión que se expresan en este documento representan nuestra visión a partir de la situación actual del mercado y están sujetas a cambios sin previo aviso.

CONSIDERACIONES SOBRE RIESGOS

- Las rentabilidades pasadas no son un indicador fiable de resultados futuros. No es posible invertir directamente en un índice.

- Los precios y las tasas de rentabilidad son indicativos, ya que pueden variar con el tiempo en función de las condiciones del mercado.

- Existen otras consideraciones sobre riesgos para todas las estrategias.

- La información que aquí se incluye no pretende ser una recomendación, ni una oferta, ni una solicitud de compra o venta de ningún producto o servicio de inversión.

- Las opiniones que aquí se manifiestan pueden diferir de las expresadas por otras áreas de J.P. Morgan. Este documento no debe considerarse un análisis de inversión ni un informe de análisis de inversión de J.P. Morgan.

INFORMACIÓN IMPORTANTE

El presente documento tiene como único fin informarle sobre determinados productos y servicios que ofrecen las divisiones de gestión de patrimonios de J.P. Morgan, integrantes de JPMorgan Chase & Co. (“JPM”). Los productos y servicios descritos, así como las comisiones, los gastos y los tipos de interés asociados, pueden sufrir modificaciones de acuerdo con los contratos de cuenta aplicables, además de diferir entre ámbitos geográficos. No todos los productos y servicios se ofrecen en todas las regiones. Lea íntegramente toda esta sección de información importante.

RIESGOS Y CONSIDERACIONES GENERALES

Las opiniones, las estrategias y los productos que se describen en este documento pueden no ser adecuados para todas las personas y comportan riesgos. Los inversores podrían recuperar menos del importe invertido, y la rentabilidad histórica no es un indicador fiable de resultados futuros. La distribución / diversificación de activos no garantiza beneficios o protección contra pérdidas. Nada de lo incluido en este documento debe utilizarse como único elemento de juicio para tomar una decisión de inversión. Se le insta a analizar minuciosamente si los servicios, los productos, las clases de activos (por ejemplo, renta variable, renta fija, inversiones alterativas y materias primas) o las estrategias que se abordan resultan adecuados en vista de sus necesidades. También debe tener en cuenta los objetivos, los riesgos, las comisiones y los gastos asociados al servicio, el producto o la estrategia de inversión antes de tomar una decisión de inversión. Para ello y para obtener información más completa, así como para abordar sus objetivos y su situación, póngase en contacto con su equipo de J.P. Morgan.

FIABILIDAD DE LA INFORMACIÓN AQUÍ INCLUIDA

Ciertos datos incluidos en este documento se consideran fiables; sin embargo, JPM no declara ni garantiza su precisión, su fiabilidad o su integridad y excluye cualquier responsabilidad por pérdidas o daños (directos o indirectos) derivados de la utilización, total o parcial, del presente documento. JPM no formula declaraciones o garantías con respecto a los cálculos, los gráficos, las tablas, los diagramas o los comentarios que pueda contener este documento, cuya finalidad es meramente ilustrativa/orientativa. Las perspectivas, las opiniones, las estimaciones y las estrategias que se abordan en este documento constituyen nuestro juicio con base en las condiciones actuales del mercado y pueden cambiar sin previo aviso. JPM no asume obligación alguna de actualizar la información que se recoge en este documento en caso de que se produzcan cambios en ella. Las perspectivas, las opiniones, las estimaciones y las estrategias que aquí se abordan pueden diferir de las expresadas por otras áreas de JPM y de las opiniones expresadas con otros propósitos o en otros contextos; este documento no debe considerarse un informe de análisis. Los resultados y riesgos proyectados se basan únicamente en los ejemplos hipotéticos citados, y los resultados y riesgos reales variarán según las circunstancias específicas. Las declaraciones prospectivas no deben considerarse como garantías o predicciones de eventos futuros.

Nada de lo indicado en este documento se entenderá que da lugar a obligación fiduciaria o relación de asesoramiento alguna hacia usted o un tercero. Nada de lo indicado en este documento debe ser considerado como una oferta, invitación, recomendación o asesoramiento (ya sea financiero, contable, jurídico, fiscal o de otro tipo) por parte de J.P. Morgan y/o sus equipos o empleados, con independencia de que dicha comunicación haya sido facilitada a petición suya o no. J.P. Morgan y sus filiales y empleados no prestan servicios de asesoramiento fiscal, jurídico o contable. Consulte a sus propios asesores fiscales, jurídicos y contables antes de realizar operaciones financieras.

INFORMACIÓN IMPORTANTE ACERCA DE SUS INVERSIONES Y POSIBLES CONFLICTOS DE INTERESES

Surgirán conflictos de interés cuando JPMorgan Chase Bank, N.A. o cualquiera de sus filiales (conjuntamente, “J.P. Morgan”) tengan un incentivo real o supuesto, de índole económica o de otro tipo, en la gestión de las carteras de nuestros clientes para actuar de un modo que beneficie a J.P. Morgan. Surgirán conflictos, por ejemplo (en la medida en que las siguientes actividades estén autorizadas en su cuenta): (1) cuando J.P. Morgan invierta en un producto de inversión, como un fondo de inversión, un producto estructurado, una cuenta de gestión discrecional o un hedge fund, emitido o gestionado por JPMorgan Chase Bank, N.A. o una filial, como J.P. Morgan Investment Management Inc.; (2) cuando una entidad de J.P. Morgan obtenga servicios, incluidas la ejecución y la compensación de operaciones, de una filial; (3) cuando J.P. Morgan reciba un pago como resultado de la compra de un producto de inversión por cuenta de un cliente; o (4) cuando J.P. Morgan reciba un pago por la prestación de servicios (incluidos servicios a accionistas, mantenimiento de registros o custodia) con respecto a productos de inversión adquiridos para la cartera de un cliente. Otros conflictos surgirán por las relaciones que J.P. Morgan mantenga con otros clientes o cuando J.P. Morgan actúe por cuenta propia.

Las estrategias de inversión se seleccionan entre las de los gestores de J.P. Morgan y las de otros gestores de activos, y son objeto de un proceso de revisión por nuestros equipos de análisis. De ese grupo de estrategias, nuestros equipos de elaboración de carteras seleccionan aquellas que consideramos adecuadas conforme a nuestros objetivos de asignación de activos y previsiones a fin de cumplir los objetivos de inversión de la cartera.

Con carácter general, preferimos las estrategias de inversión gestionadas por J.P. Morgan. Esperamos que el porcentaje de estrategias gestionadas por J.P. Morgan sea alto (de hecho, hasta de un 100%) en estrategias como, por ejemplo, de liquidez y renta fija de alta calidad, sujeto a la legislación vigente y a cualesquiera consideraciones específicas de la cuenta.

Si bien nuestras estrategias de gestión interna suelen estar bien alineadas con nuestras previsiones y estamos familiarizados con los procesos de inversión y con la filosofía de riesgos y cumplimiento de la firma, debemos señalar que J.P. Morgan percibe en conjunto más comisiones cuando se incluyen estrategias gestionadas internamente. Ofrecemos la opción de excluir estrategias gestionadas por J.P. Morgan (que no sean productos de efectivo y liquidez) en determinadas carteras.

Los fondos Six Circles son fondos de inversión inscritos en Estados Unidos gestionados por J.P. Morgan y, a su vez, cuya gestión se ha delegado en terceros. Aunque se consideran estrategias gestionadas a escala interna, JPMC no cobra comisiones por gestionar los fondos o prestar otros servicios conexos.

PERSONAS JURÍDICAS, MARCAS E INFORMACIÓN REGULATORIA

En Luxemburgo, este documento lo emite J.P. Morgan Bank Luxembourg S.A. (JPMBL), con domicilio social en European Bank and Business Centre, 6 route de Trèves, L-2633, Senningerberg (Luxemburgo). Inscrita en el Registro mercantil de Luxemburgo con el número B10.958. Autorizada y regulada por la Commission de Surveillance du Secteur Financier (CSSF) y supervisada conjuntamente por el Banco Central Europeo (BCE) y la CSSF. J.P. Morgan Bank Luxembourg S.A. se encuentra autorizada como entidad de crédito de acuerdo con la Ley de 5 de abril de 1993. En el Reino Unido, este documento lo emite J.P. Morgan Bank Luxembourg S.A., London Branch, con domicilio social en el 25 Bank Street, Canary Wharf, Londres E14 5JP. Autorizada y regulada por la Commission de Surveillance du Secteur Financier (CSSF) y supervisada conjuntamente por el Banco Central Europeo (BCE) y la CSSF. Autorizada por la Prudential Regulation Authority. Sujeta a la regulación de la Financial Conduct Authority y a la regulación limitada del Prudential Regulation Authority. Los detalles del Régimen de Licencias Temporales, que permiten a las entidades domiciliadas en el Espacio Económico Europeo operar temporalmente en el Reino Unidomientras solicitan la autorización completa están disponibles en la página web de la Financial Conduct Authority. En España, este documento lo distribuye J.P. Morgan Bank Luxembourg S.A., Sucursal en España, con domicilio social en Paseo de la Castellana, 31, 28046 Madrid (España). J.P. Morgan Bank Luxembourg S.A., Sucursal en España se encuentra inscrita con el número 1516 en el registro administrativo del Banco de España y supervisada por la Comisión Nacional del Mercado de Valores (CNMV). En Alemania, este documento lo distribuye J.P. Morgan Bank Luxembourg S.A., Frankfurt Branch, con domicilio social en Taunustor 1 (TaunusTurm), 60310 Frankfurt (Alemania), supervisada conjuntamente por la Commission de Surveillance du Secteur Financier (CSSF) y el Banco Central Europeo (BCE), supervisada asimismo en determinadas áreas por la Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin). En Italia, este documento lo distribuye J.P. Morgan Bank Luxembourg S.A., Milan Branch, con domicilio social en Via Cordusio 3, Milán 20123 (Italia) y regulada por el Banco de Italia y la Commissione Nazionale per le Società e la Borsa (CONSOB). En Paises Bajos este documento lo distribuye J.P. Morgan Bank Luxembourg S.A., Amsterdam Branch, con domicilio social en World Trade Centre, Torre B, Strawinskylaan 1135, 1077 XX, Amsterdam, Paises Bajos. J.P. Morgan Bank Luxembourg S.A., Amsterdam Branch está autorizada y regulada por la Commission de Surveillance du Secteur Financier (CSSF) y supervisada conjuntamente por el Banco Central Europeo y la CSSF en Luxembourg; J.P. Morgan Bank Luxembourg S.A., Amsterdam Branch está también autorizada y supervisada por De Nederlandsche Bank (DNB) y la Autoriteit Financiële Markten (AFM) en Paises Bajos. Se encuentra registrada ante la Kamer van Koophandel como sucursal de J.P. Morgan Bank Luxembourg S.A. con el número 71651845. En Dinamarca este document lo distribuye J.P. Morgan Bank Luxembourg, Copenhagen Br, sucursal de J.P. Morgan Bank Luxembourg S.A. con domicilio social en Kalvebod Brygge 39-41, 1560 København V, Dinamarca. J.P. Morgan Bank Luxembourg, Copenhagen Br, sucursal de J.P. Morgan Bank Luxembourg S.A. está autorizada y regulada por la Commission de Surveillance du Secteur Financier (CSSF) y conjuntamente supervisada por el Banco Central Europeo y la CSSF. J.P. Morgan Bank Luxembourg, Copenhagen Br, sucursal de J.P. Morgan Bank Luxembourg S.A. está también supervisada por la Finanstilsynet (FSA Danesa) y registrada con la Finanstilsynet como una sucursal de J.P. Morgan Bank Luxembourg S.A. bajo el código 29009. En Suecia, este material lo distribuye J.P. Morgan Bank Luxembourg S.A. - Stockholm Bankfilial, con domicilio social en Hamngatan 15, Stockholm, 11147, Suecia. J.P. Morgan Bank Luxembourg S.A. - Stockholm Bankfilial está autorizada y regulada por la Commission de Surveillance du Secteur Financier (CSSF) y supervisada conjuntamente por el Banco Central Europeo y la CSSF. J.P. Morgan Bank Luxembourg S.A., Stockholm Branch está también sujeta a la supervison de Finansinspektionen (FSA Sueca). Está registrada con la Finansinspektionen como una sucursal de J.P. Morgan Bank Luxembourg S.A.. En Francia este documento también puede distribuirlo JPMorgan Chase Bank, N.A. (“JPMCB”), Paris Branch, regulada por las autoridades bancarias francesas (Autorité de Contrôle Prudentiel et de Résolution y Autorité des Marchés Financiers). En Suiza, el material es distribuido por J.P. Morgan (Suisse) SA, con domicilio en rue de la Confédération, 8, 1204, Ginebra, Suiza, y que está autorizada y supervisada por la Autoridad Suiza de Supervisión de Mercados Financieros (FINMA), con domicilio en Laupenstrasse 27, 3003, Berna, Suiza, como banco y sociedad de valores en Suiza. Consulte el siguiente enlace para obtener información relativa a la política de protección de datos en EMEA de J.P. Morgan: https://www.jpmorgan.com/privacy.

Esta comunicación es un anuncio a los efectos de la Directiva sobre mercados de instrumentos financieros (MIFID II) y la Ley de servicios financieros de Suiza (FINSA). Los inversores no deben suscribir ni comprar ningún instrumento financiero mencionado en este documento, excepto sobre la base de la información contenida en cualquier documentación legal aplicable, que esté o estará disponible en las jurisdicciones pertinentes.

Con respecto a los países de América Latina, la distribución de este documento puede estar restringida en ciertas jurisdicciones. Es posible que le ofrezcamos y/o le vendamos valores u otros instrumentos financieros que no puedan registrarse y no sean objeto de una oferta pública en virtud de la legislación de valores u otras normativas financieras vigentes en su país de origen. Tales valores o instrumentos se le ofrecen y/o venden exclusivamente de forma privada. Las comunicaciones que le enviemos con respecto a dichos valores o instrumentos —incluidos, entre otros, un folleto, un pliego de condiciones u otro documento de oferta— no tienen como fin constituir oferta de venta o invitación para comprar valores o instrumentos en ninguna jurisdicción en que dichas oferta o invitación sean ilegales. Además, la transferencia posterior por su parte de dichos valores o instrumentos puede estar sujeta a ciertas restricciones regulatorias y/o contractuales, siendo usted el único responsable de verificarlas y cumplirlas. En la medida en que el contenido de este documento haga referencia a un fondo, el fondo no podrá ofrecerse públicamente en ningún país de América Latina sin antes registrar los títulos del fondo de acuerdo con las leyes de la jurisdicción correspondiente. Queda terminantemente prohibida la oferta pública de cualquier título, incluidas las participaciones del fondo, que no se haya registrado previamente ante la Comisión de Valores y Mercados (CVM) de Brasil. Es posible que las plataformas de Brasil y de México no ofrezcan actualmente algunos de los productos o servicios incluidos en este documento.

Las referencias a “J.P. Morgan” remiten a JPM, sus sociedades dependientes y sus filiales de todo el mundo. “J.P. Morgan Private Bank” es el nombre comercial de la división de banca privada de JPM.

Este documento tiene como fin su uso personal y no debe distribuirse a, ni ser utilizado por, otras personas, ni ser copiado para fines no personales sin nuestro permiso. Si tiene alguna pregunta o no desea continuar recibiendo estas comunicaciones, no dude en ponerse en contacto con su equipo de J.P. Morgan.

© 2022 JPMorgan Chase & Co. Todos los derechos reservados.