Investment Strategy

The five most popular investing mistakes of 2024

It’s easy to get emotional about money. Various behavioral biases—such as overconfidence, loss aversion and bandwagon-jumping—can push investors into making decisions that undermine their efforts to reach their goals.

This might be especially true today in a market with recent memories of a pandemic, generationally high inflation, simultaneous stock and bond market routs, and recession fears. Those events have left a strong imprint on investors’ behavior, and the effects aren’t always positive.

At the Private Bank, we’re focused on helping our clients achieve their goals for their wealth, and we’ve uncovered a few common mistakes we see investors making today. By staying mindful of these, we just might be better equipped to overcome them.

1. Cashing out when markets get volatile

Volatility is a feature of investing, not a bug: Since 1980, the S&P 500 has suffered average intra-year pullbacks of -15%. In 16 of the 44 years, the index experienced even steeper losses.

Still, drawdowns and all, full-year returns ended up positive 75% of the time (or in 33 of those years). The advice to “stay invested” when the going gets tough might be considered a reductive cliché, but it’s not. The data shows that it tends to pay off over the long run. And diversifying your portfolio with the addition of core bonds could help cushion against equity market volatility and smooth out the ride.

Despite intra-year swings, equities tend to reward investors

S&P 500 intra-year declines (max drawdowns) & calendar year price returns

Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management—Guide to the Markets. Returns are based on price index only and do not include dividends. Intra-year drops refer to the largest market drops from a peak to a trough during the year. Return shown are calendar year returns from 1980 to present year. Data as of February 1, 2024.

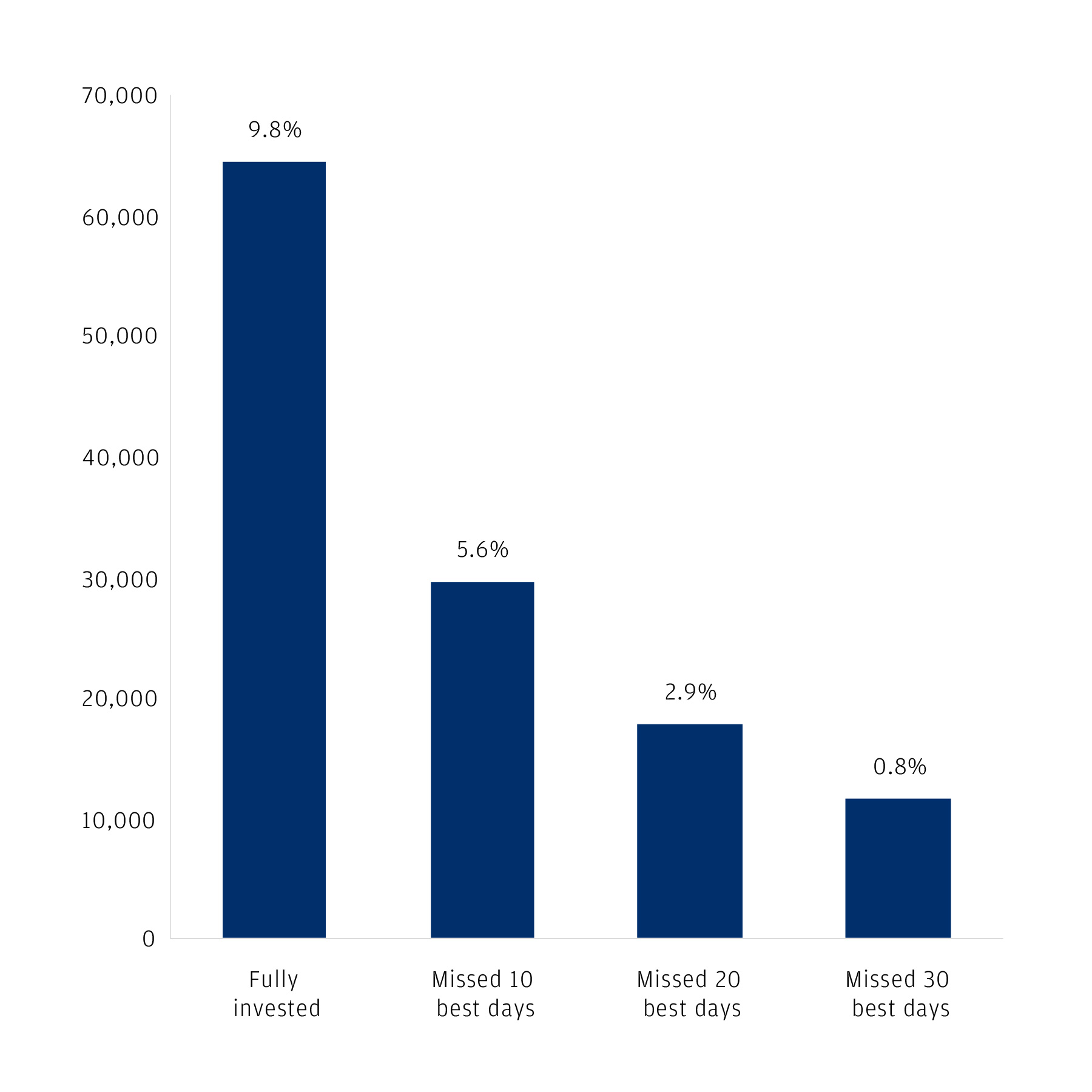

2. Trying to time the market

In a perfect world, investors would always buy at the low and sell at the high, consistently maximizing returns and minimizing their regrets. Maybe you think you can time the market better than the average investor, and maybe you’re right. But consider the risks.

The chart below illustrates what would happen if an investor missed the 10 single best days in the equity markets over the past 20 years. The end value of the hypothetical investor’s portfolio would be cut by more than half. If missing the 10 best days sounds implausible to you, consider that in the past 20 years, seven of those best days happened within 15 days of the 10 worst days. An investor who got out of the market around those worst days might not be willing to get back in that quickly.

The bottom line: Timing the market is a lot harder than it may seem, and the consequences of getting it wrong can be significant.

Performance of the S&P 500: Missing the best days

Annualized performance of a $10,000 investment from January 2004 through January 2024

Source: J.P. Morgan Asset Management analysis using data from Morningstar Direct. Returns are based on the S&P 500 Total Return Index, an unmanaged, capitalization-weighted index that measures the performance of 500 large capitalization domestic stocks representing all major industries. Past performance is not indicative of future returns. An individual cannot invest directly in an index. Analysis is based on the J.P. Morgan Guide to Retirement. Data as of February 1, 2024.

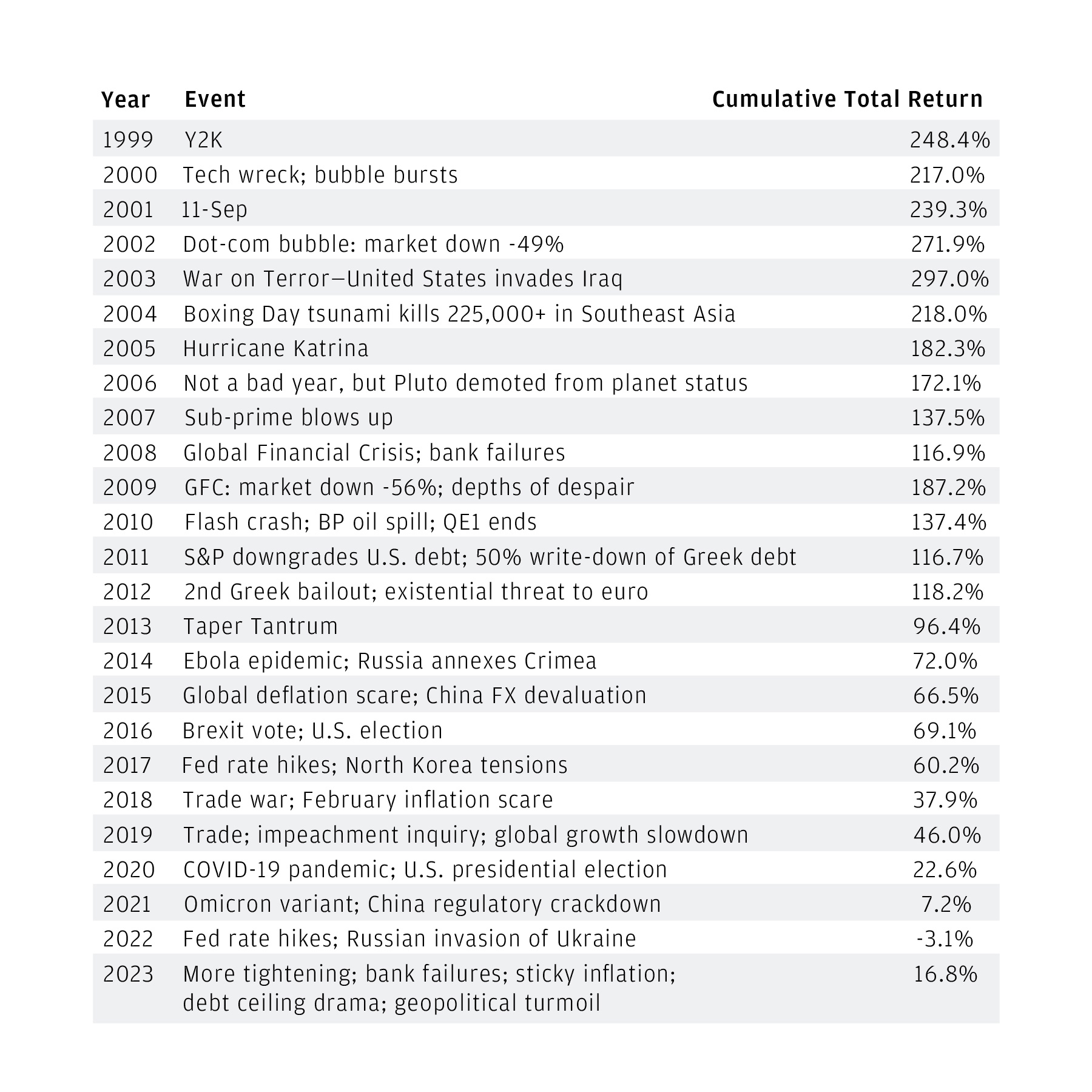

3. Chasing headlines instead of sticking to the plan

In 2021, “meme stock” madness minted millionaires seemingly overnight. Fear of missing out drove troves of investors into stocks such as GameStop as they rocketed higher, and many of them took losses when the stocks crashed in the subsequent weeks. More recently, many investors feared a recession in 2023 and hid out in the safety of cash. Those who did missed out on broad global equity gains, as the benchmark MSCI World Index climbed +24% over the course of the year.

Whether amid hype or hysteria, humans have a knack for fixating on near-term dynamics that might prompt emotional decisions that ultimately derail their longer-term goals. Making a plan is easy, but staying with it is hard. Recognizing our tendency to chase headlines is the first step in avoiding that mistake.

After all, history has shown that investing in a diversified portfolio aligned with your time horizon and risk tolerance, and sticking with it, tends to be an effective way to grow your money over time—regardless of the risk du jour. The table illustrates this fundamental principle of investing. There are always global events and risks that might persuade an investor to get out of the market—and to stay out for longer and longer until things improve. But an investor who stays in the market, even through hard times, ultimately reaps the rewards.

Some examples of reasons not to invest

Source: J.P. Morgan, FactSet. Cumulative total returns for the 60/40 portfolio (net total return for MSCI World and Bloomberg Global Aggregate Indexes) are calculated from December 31 of the year prior until the updated data. Data as of January 31, 2024.

4. Trying to do it all themselves

Tactics like tax minimization can offer major benefits, helping investors keep more of what they’ve earned. Many investors achieve this through tax-loss harvesting, where assets trading at a loss are sold to help offset capital gains in other parts of the portfolio.

Not so long ago, maximizing the effectiveness of this approach required investors to have the time, discipline and desire to carefully track every position in their accounts on a daily basis to identify every single opportunity to harvest tax losses (and avoid violating wash sale rules1). Today, there is robust technology that can monitor accounts daily to capture losses more consistently and amplify your portfolio’s tax efficiency.

Active managers' outperformed their benchmark at a larger percentage in small cap and international markets

Percentage of active funds in select equity categories that outperformed their benchmark indices (March 2018-March 2023)

Source: Morningstar, J.P. Morgan Private Bank; data as of March 31, 2023. Performance is net of underlying fund expense ratio. Study covered more than 3,000 active mutual funds and ETFs. Equity categories selected are the 9 largest in Morningstar by AUM on our platform. Past performance is not indicative of future results.

In a similar vein, effective active management can generate outperformance versus broad markets that compounds to meaningful gains over time. We can help you decide where it might make the most sense to use it.

5. Taking risks that don’t suit their goals

When it comes to your money, what does “risk” mean to you?

It might bring to mind geopolitical conflicts, bankruptcies, supply chain snarls or asset bubbles, and the market selloffs they can cause. But do you also think of risks such as outliving your money, losing purchasing power to inflation or not having enough liquidity on hand to address an unforeseen circumstance?

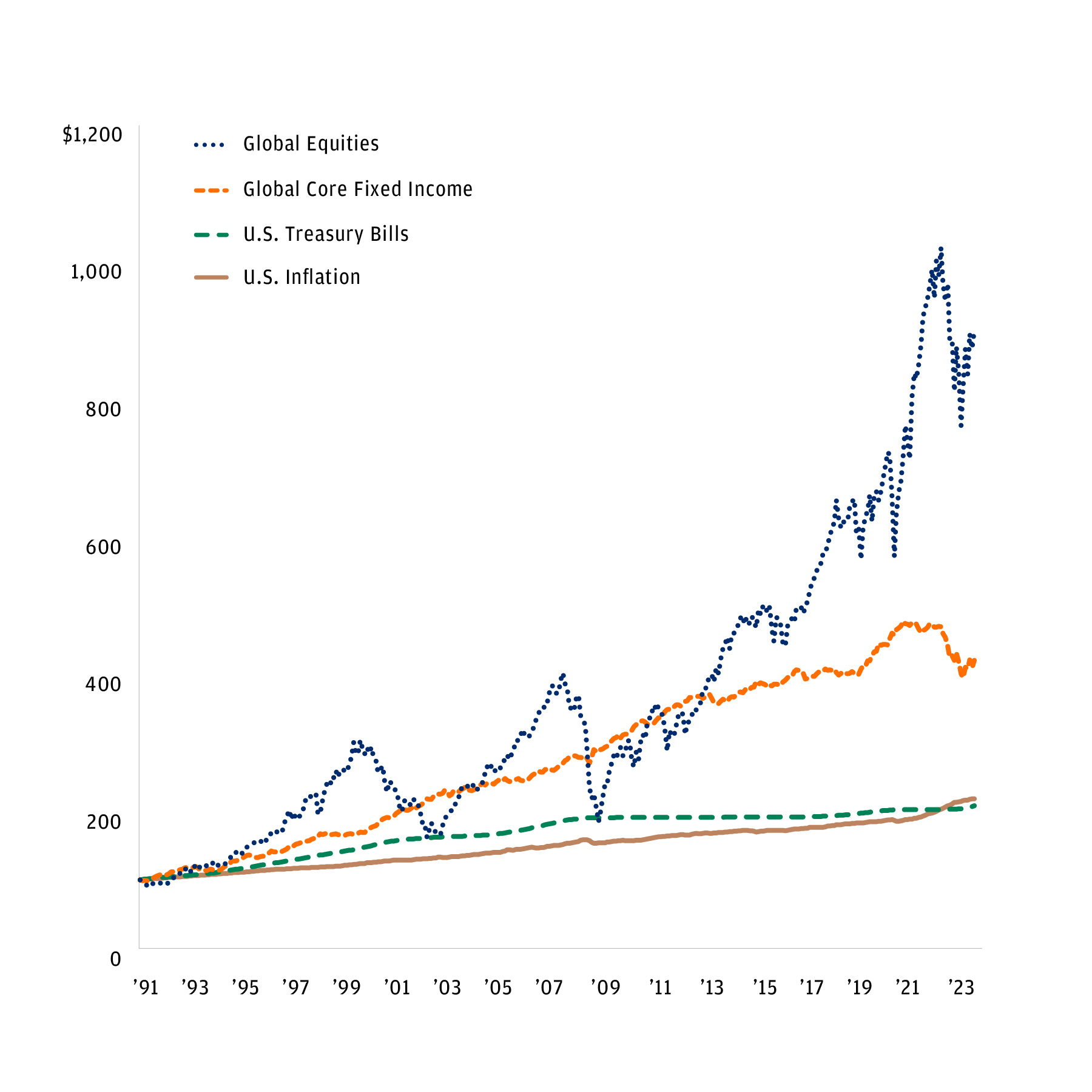

Every asset allocation decision comes with tradeoffs. For example, cash may satisfy our wish to avoid losses during market drawdowns, but over the past 30 years, it has generated next to no inflation-adjusted return. Stocks, on the other hand, have historically been the reliable engine of meaningful capital appreciation over longer, multi-year time horizons, but their volatility makes them a hazardous place to park money you may need to spend in the months ahead.

This is why we encourage clients to engage in a comprehensive planning process. By dividing your wealth into sleeves with specific purposes, from day-to-day spending to leaving a long-term legacy, you can make better choices about the risk tradeoffs you are willing to take to achieve your financial goals.

Equities and fixed income have outperformed cash and inflation

Growth of $100 in various assets and inflation from 1991

Source: Bloomberg Finance L.P., J.P. Morgan Asset Management—2024 Long-Term Capital Market Assumptions (LTCMAs). Global equities represented by MSCI World USD Total Return Index, U.S. core fixed income by Bloomberg U.S. Investment Grade Bond Index, U.S. Treasury bills by Bloomberg U.S. Treasury Bill 1–3 months Index, U.S. inflation by U.S. Headline Consumer Price Index (CPI). Historical data as of January 31, 2024. LTCMA projections as of September 30, 2023.

We can help

No one is immune from investing mistakes, so if any of these missteps feel familiar, know you’re not alone. There isn’t much we can do to control the environment in which we invest. But there is plenty we can control by focusing on specific goals, identifying what it will take to meet them, and forming and following a plan. We’re here to help you navigate that process. Contact your J.P. Morgan team to learn more.

1The wash sale rules state, in essence, that a loss will be disallowed if the taxpayer sells a security at a loss, and acquires the same or a substantially identical security (or an option on such security) within 30 days on either side of the date the loss was realized. The disallowed loss is then added to the cost basis of the substantially identical acquired security and generally recognized when the position is later sold.

From staying in cash to going it alone, here are the most worrying errors we’re seeing investors make at the start of 2024.

Elyse Ausenbaugh

Global Investment Strategist

Published Mar 7, 2024

EXPERIENCE THE FULL POSSIBILITY OF YOUR WEALTH

We can help you navigate a complex financial landscape. Reach out today to learn how.

Contact us